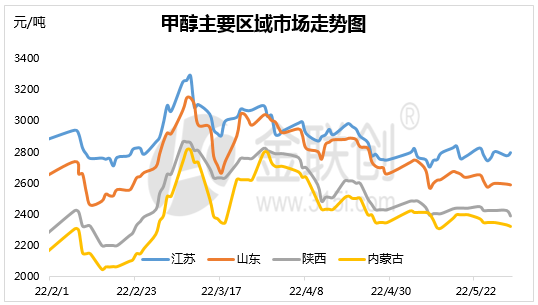

In May, China;s methanol market continued to fluctuate and move lower; During this period, commodities from the macro, crude oil, coal, epidemic and other external driving factors continued to strengthen, and in the background of weak economy, macro news frequently stimulated the commodity market, and the market transmission from futures, ports and the mainland showed obvious disturbance. In addition, the implementation of dual-track coal, chemical coal for methanol cost support still exist. Back to the fundamentals, the methanol project in this month is on and off, the overall supply fluctuation is limited; However, import increment is gradually reflected, and the base difference of the port is obviously weakened this month under the expectation of the bank. At the demand end, the demand of various production areas increased and decreased, and some olefin stages of negative/stopping had a slight fluctuation on the market.

Supply side: The methanol industry started 73.7% in May, down 0.26 percentage points from the previous month. In addition to the seasonal routine maintenance, in May fault shutdown/negative drop, Sichuan and Chongqing phase gas restriction led to slightly reduced supply to the construction of constraints. In terms of supply in June, although some devices are still expected to have planned maintenance (such as: Runzhong, Luhua and Hebei Huafeng planned maintenance at the end of May, Northwest Energy Source, Shanghai Coking, Mingshui and other planned maintenance in June), the overall quantity involved is reduced, and superposition the return of maintenance projects in May, partial air head recovery in early June, etc., so it is expected that the overall supply of inner disk is still sufficient. In addition, the expected simultaneous overhaul of methanol and olefin storage in Yulin, Shaanxi Province in June has a relatively small impact on the commercial volume of methanol. In June, Anhui and Ningxia paid attention to the pace of new devices. In conclusion, it is expected that the local supply of methanol will increase with a high probability in June. It is necessary to continue to pay attention to whether the cost end of coal will have an impact on the start-up fluctuations of some projects. In terms of imports, China's methanol import volume continued to increase in April, mainly due to stable international supply and increased domestic unloading rate. The import volume in May is expected to be around 1.2-1.23 million tons. In June, shipments from Iran remained stable, and goods from Iran and other places in Central and East Africa were mainly delivered for a long time, while the overall supply was stable. Under the influence of external factors such as unblocked shipping, China's methanol import volume in June is expected to be slightly reduced to around 1.1 million tons.

Demand side: The overall demand performance of methanol downstream was weak in May. Although there was an increase in the production of formaldehyde and MTBE, the overall increase was not large. In addition, the construction of olefin, dimethyl ether, acetic acid, DMF and BDO all declined. Although the epidemic situation in Shanghai gradually improved and the resumption of work and production was gradually promoted, the performance of end demand and consumer consumption was still mediocre under the background of weak economy. Therefore, it was still necessary to pay close attention to the beneficial and multiple transmission effect of macroeconomic stimulus on demand side in June. In terms of the overall demand in June, the increment of demand at the olefin end may be limited. Although Yangcoal is preliminarily expected to recover around June 10, the delayed restart of Chengzhi Phase I, low load of Ningbo project and slight fluctuation of Zhapu at the end of May will still affect the start of the industry. In addition, we need to pay attention to the implementation of maintenance in June in Luxi, Shaanxi Yulin Coal. From the traditional downstream point of view, June to July with the increase of rain, superimposed real estate market performance is poor, formaldehyde, plate demand will gradually enter the seasonal off-season; Although Nanjing Ineos is expected to recover the acetic acid in June, but Yanmine, Celanese, Shanghai Huayi are planned to overhaul, this kind of downstream demand may still be in a state of shrinkage. In terms of MTBE, stimulated by large export profits, Lu Shenfa and China Savings restarted their expectations in June, focusing on the stimulation and transmission of raw material methanol; We are also concerned about the resumption of the Black Cat, Xinye and Cathay Pacific Xinhua BDO projects in early June. To sum up, the overall demand for methanol in June may still be relatively average, and some industries are still facing reduction expectations.

In general, while the domestic methanol in June was alert to the intensified game between supply and demand, the cost changes of coal, the intensity and pace of macroeconomic stimulus and other drivers still need continuous attention. It is expected that the overall market will continue to be weak, and the risk of local declines still exists. First of all, methanol spring test support margin gradually weakened, the shrinkage caused by maintenance and gas restriction will gradually return; Superimposed low cost import source inflow is sufficient, the overall supply of internal and external disk performance is rich; And the inner disk new device release expectations, the outer disk hanging highlights also need to pay attention to. Secondly, the demand end may face corresponding shrinkage, such as the olefin performance is normal, traditional downstream seasonal off-season, etc. Therefore, it is expected that under the background of weak economic environment, the contradiction between methanol supply and demand still exists in June, and the overall market is relatively weak and the probability of falling is relatively large.